(Bloomberg) — U.S. businesses and consumers started the year thinking interest rates would finally fall, making big plans to buy equipment or a home. Now all of that is on hold, slowing large parts of the economy for the foreseeable future.

Most read on Bloomberg

In Michigan, a cutting tool manufacturer deferred up to $1 million in spending on new equipment this year. In Atlanta, a woodworking machine manufacturer says some customers are trying to extend the life of a device.

When progress on inflation stalled earlier this year and Federal Reserve officials decided to keep rates at 23-year highs for longer, it forced businesses to rethink their investments in capital expenditures, inventory and hiring. On Wednesday, policymakers are expected to keep borrowing costs stable again after their two-day policy meeting in Washington.

For businesses, the problem manifests itself in the data. S&P Global Market Intelligence forecasts that capital investment in manufacturing will increase only 3.9% this year, compared to an estimate of 6.7% in January. In the United States, business bankruptcy filings increased more than 40% over the past year through the end of March, while personal bankruptcy filings increased 15%, according to the US Administrative Office. American courts.

In a June 5 report from the Institute for Supply Management, a majority of service sector respondents indicated that current inflation and interest rates are hindering improved business conditions. That's after expressing optimism in January about the potential impact of interest rate cuts, Anthony Nieves, chairman of the ISM Services Business Investigation Committee, said in statements.

The Fed's decision to keep interest rates higher than expected is also sowing uncertainty around the world, while further squeezing debt-strapped consumers and delaying home purchases.

Delayed equipment purchases

“You definitely have to take the reins off when interest rates are high,” said Patrick Curry, president of Michigan-based Fullerton Tool Co.. “We have to wait out some of that and try to make the most of the existing equipment that we have. to have.”

With two factories in Saginaw, Michigan, and one in California making cutting tools for the aerospace, automotive and medical fields, among others, Fullerton, 81, has delayed spending on 'about $1 million to upgrade its equipment and customers aren't buying as much. equipment, Curry said.

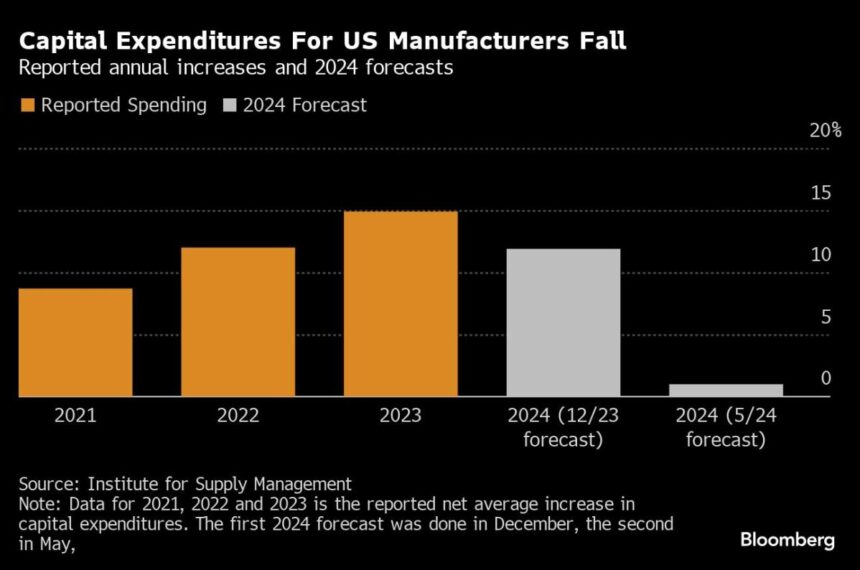

The ISM's May 15 economic forecast showed that business executives expect only a 1% increase in capital spending this year, down from their December 2023 estimate of nearly 12%.

Investors are pricing in about 1.5 rate cuts this year, giving roughly equal chances for a first cut in September, according to futures contracts.

If the Fed begins cutting rates on that date, investment in business and software should pick up in the latter part of the year, Leigh Lytle, chief executive of the Equipment Leasing and Finance Association, said in a statement. .

Just north of Atlanta, there is still demand for the heavy saws and drills used to make cabinets and furniture, said Blair Chandler, manager of equipment financing and leasing at SCM North America, a manufacturer of woodworking machines.

While larger customers continue to make purchases, the company's smaller customers are trying to extend the life of their old equipment, Chandler said.

“I've seen small businesses spend money on maintaining their equipment, and they have to convince themselves to buy this new equipment,” she added.

Rising borrowing costs

Small businesses are also buckling under the pressure of high borrowing rates, persistent inflation and wages, which continue to grow at more than 4% a year, according to government data through May.

About 6% of small businesses said financing was their top business issue in May, the highest proportion in nearly 14 years, according to the National Federation of Independent Business. Default rates on small business loans hit an annual rate of 3.2% in April, matching their highest level in at least a decade, according to credit bureau Equifax.

Businesses are also feeling the effects of variable rate mortgages.

Loan rates at Gastamo Group, a Denver-based restaurant company, will double to 8 percent starting in two years. That's no small feat: The company has loans of up to $3 million on some of its properties, said Peter Newlin, the company's chief vision officer.

Even if the loans don't reset immediately for a year or more, “they're coming,” Newlin said.

Read: US homeowners with adjustable mortgages face $1,000 per month hike

Meanwhile, rents are rising by up to 30% at properties leased by the Gastamo Group, which Newlin attributes to landlords passing on their own higher borrowing costs. This comes as customers cut back on spending after a record year in 2023, Newlin said.

In Tampa, Florida, Dilip Kanji, longtime owner of hotel company Impact Properties, has suspended plans to build three new hotels until borrowing costs fall. Interest rates on construction loans have climbed from about 5% to 9%. Given that Kanji plans to fund approximately $42 million of a total combined cost of $60 million, that's a considerable increase.

Like other hoteliers, he has renewed loans on some of his properties at much higher rates and can afford the cost for now. But he's going to play it safe. “We’re just waiting for a bit of debt relief to get these projects going.”

The pain continues

For American households, debt reached a record $17.7 trillion in the first quarter of 2024, according to a recent report from the New York Fed.

Consumers believe their financial difficulties will continue. Only about a quarter of respondents to the University of Michigan Consumer Confidence Survey now expect interest rates to fall this year, down from 32% in April.

Among businesses, expectations are equally bleak. On June 2, the ISM manufacturing report showed a further contraction in US factory activity in May.

In a call with reporters after the report's release, Timothy Fiore, chairman of the ISM Manufacturing Survey Committee, said: “Uncertainty is the devil of business, and that's exactly where we where we are today. »

–With the help of Claire Ballentine and Marie Monteleone.

(Updated with the latest NFIB data in the second paragraph under “Increase in Borrowing Costs” and in the third chart)

Most read from Bloomberg Businessweek

©2024 Bloomberg LP