Average prices charged for goods and services rose worldwide at a slightly accelerated pace in May, reflecting continued high increases in service prices combined with accelerating price growth in the manufacturing sector. However, there are signs of a slowdown in inflation in Europe. In the United States, PMI data is consistent with inflation moving closer to the Fed's target in the coming months.

Persistent global price inflation

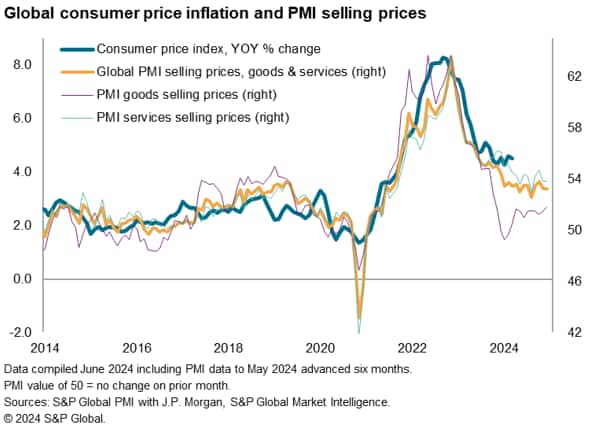

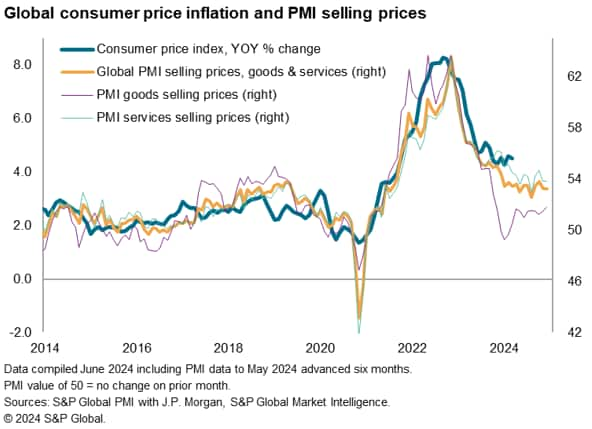

Global PMI survey data compiled by S&P Global for JP Morgan showed that average prices charged for goods and services rose globally at a slightly higher rate in May. The Composite PMI Price Loaded Index rose slightly to 53.3 from 53.2 in April, just below the 53.4 average seen over the past year – a period which saw the he index stuck in a narrow range and stubbornly high by historical standards. For comparison, this index averaged just 51.2 in the decade before the pandemic; a time when global consumer price inflation averaged 2.7%. Recent PMI figures are consistent with global inflation of around 3.5%.

While PMI data tends to trail changes in the annual rate of global consumer price inflation by about six months, the PMI's suggestion is that global inflation appears likely to remain high by standards. historic events as we head into the second half of the year. 2024.

Stubborn inflation in the services sector accompanied by rising prices of goods

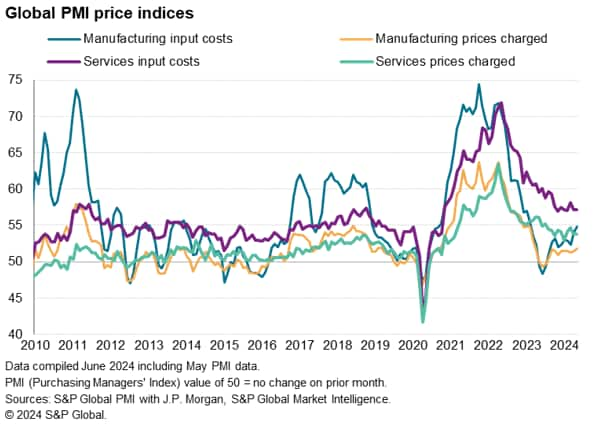

The main area of persistent price pressure globally remains the services sector, where the inflation rate remained unchanged in May at a rate well above the pre-pandemic average, although sharply down from a year ago and well below the peaks seen during the pandemic. Global service sector input cost inflation – a major component of which is wages and salaries – also remained unchanged from April in May, also standing well above its pre-retirement average. pandemic.

It is also discouraging news in the global fight against manufacturing inflation. Average prices charged for goods rose worldwide at the fastest pace in 14 months in May. Good prices have increased for ten consecutive months, driven by a proportional increase in factory input costs. Notably, prices have risen at a significantly higher rate so far in the second quarter, with the rate of input price inflation hitting a 15-month high in May, pointing to a possible further acceleration in price inflation sales in the coming months, as companies seek to pass on higher costs to customers.

In short, global services inflation remains stuck at a persistently high level by historical standards, and the beneficial disinflationary impact of manufacturing is being replaced by further upward pressure on goods prices.

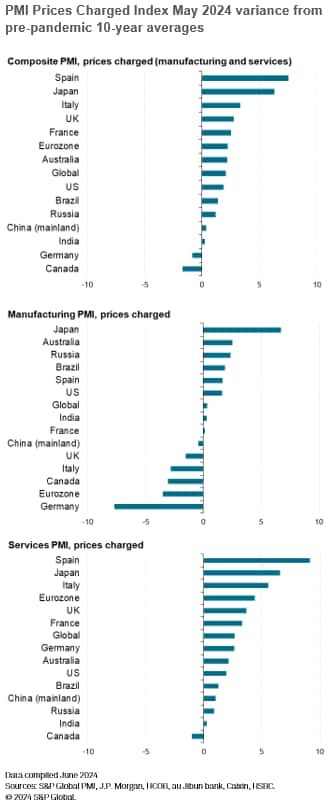

Japan, Spain and the United Kingdom experience the highest sales price inflation

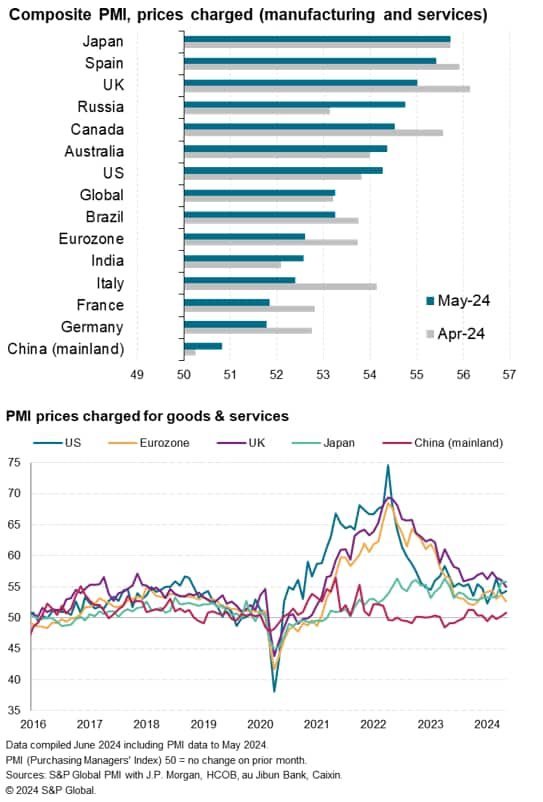

Geographically, particularly high sales price inflation rates were recorded in Japan, Spain and the United Kingdom in May, with Spain's result contrasting sharply with the average below 50.0 before the pandemic, mainly thanks to service sector inflation. Sales price inflation rates nevertheless slowed across the eurozone to their lowest level in six months, while rates eased in the four largest member states. The rate of increase also moderated in the United Kingdom, falling to its lowest level in 39 months. The PMI sales price index now stands just 2.2 points above its decade-long pandemic average in the Eurozone (and is notably 0.8 points below the pre-pandemic average in Germany) , and is 2.7 points higher in the United Kingdom.

Contrary to the easing trend seen in Europe, sales price inflation increased slightly in the United States, still sitting just 1.9 points above its ten-year average before the pandemic. Input cost inflation has also increased in the United States, both for services and goods, with the latter now reaching its highest level in 13 months.

Europe is therefore seeing signs of high inflation rates approaching ranges that would encourage central banks to feel reassured that targets are being met at sustainable degrees, but the flow of data in the coming months will be important for build confidence in this assessment. In the United States, although even at current levels the PMI index suggests further downward pressure on the Fed's preferred core PCE price indicator, progress in reducing inflation appears less some given the recent rise in input costs.

Meanwhile, the weakest price growth of the world's largest economies was again recorded in mainland China, although the rate of increase here reached its highest level in seven months, just above average of the pre-pandemic decade.

Chris Williamson, chief business economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2024, S&P Global. All rights reserved. Total or partial reproduction without authorization is prohibited.

Purchasing Managers' Index™ (PMI®) data is compiled by S&P Global for more than 40 economies around the world. Monthly data are derived from surveys of senior executives of private sector companies and are available by subscription only. The PMI dataset includes a main figure, which indicates the overall health of an economy, and sub-indexes, which provide insight into other key economic factors such as GDP, inflation, exports, capacity utilization, employment and stocks. PMI data is used by financial and business professionals to better understand where economies and markets are heading and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.