Money supply is a very important indicator. This helps show how tight or loose current monetary conditions are, regardless of the Fed's interest rate policy. Even if the Fed is restrictive, if the money supply increases, it has an inflationary effect.

One of the key indicators shown below is the 13-week annualized “Wenzel” money supply figure. It was made popular by the late Robert Wenzel who tracked the measure every week as an indicator of where the economy might be heading. In 2020, the Fed began releasing data monthly rather than weekly. It is also worth noting that money supply data could be revised sharply in the coming months.

Recent trends

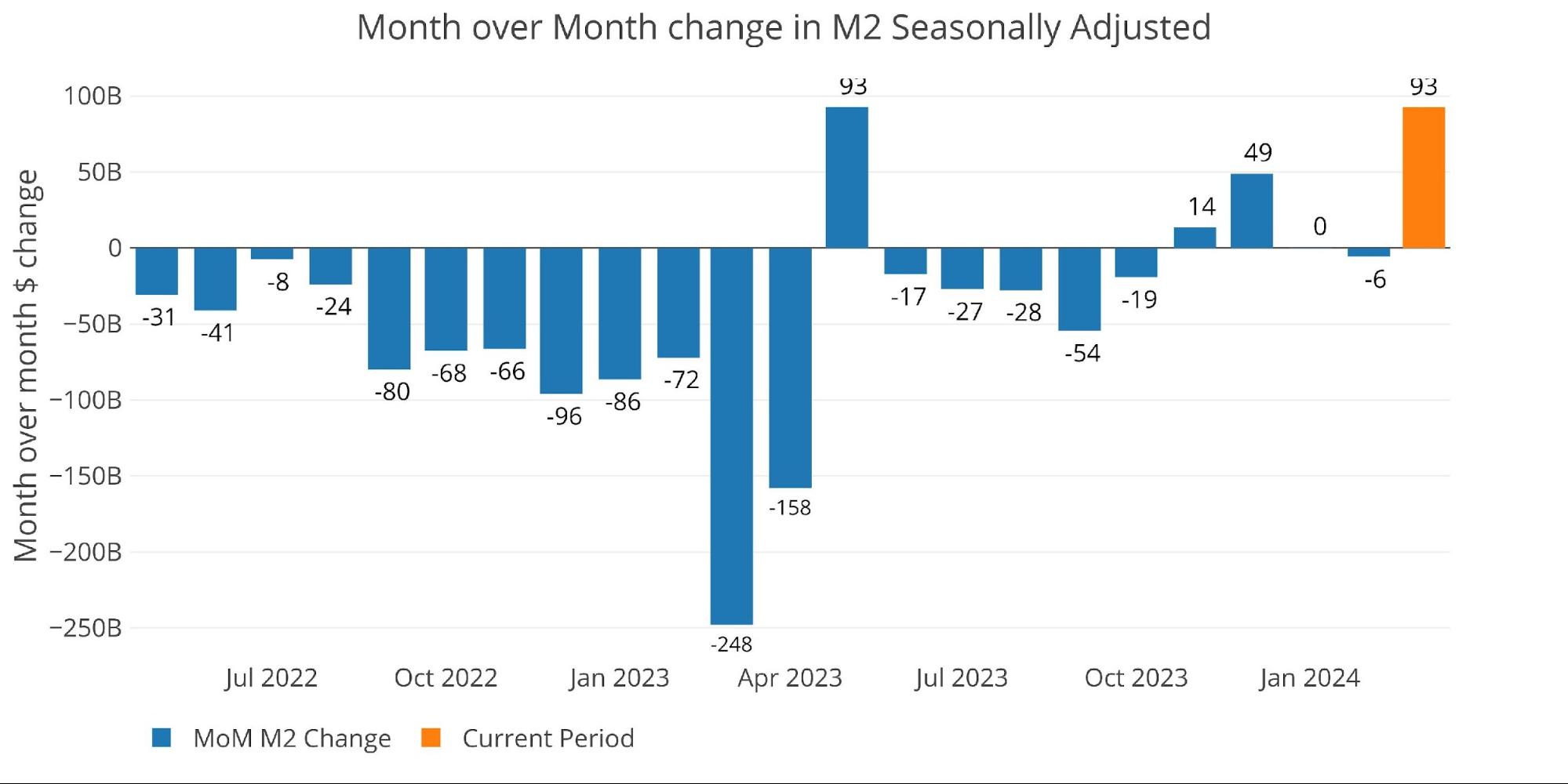

The seasonally adjusted money supply is lagged by one month. The large increase in seasonally adjusted money supply shown below occurred in March.

Figure: 1 monthly variation of M2 (seasonally adjusted)

The month of March was a strong increase with an annualized increase of 5.5%.

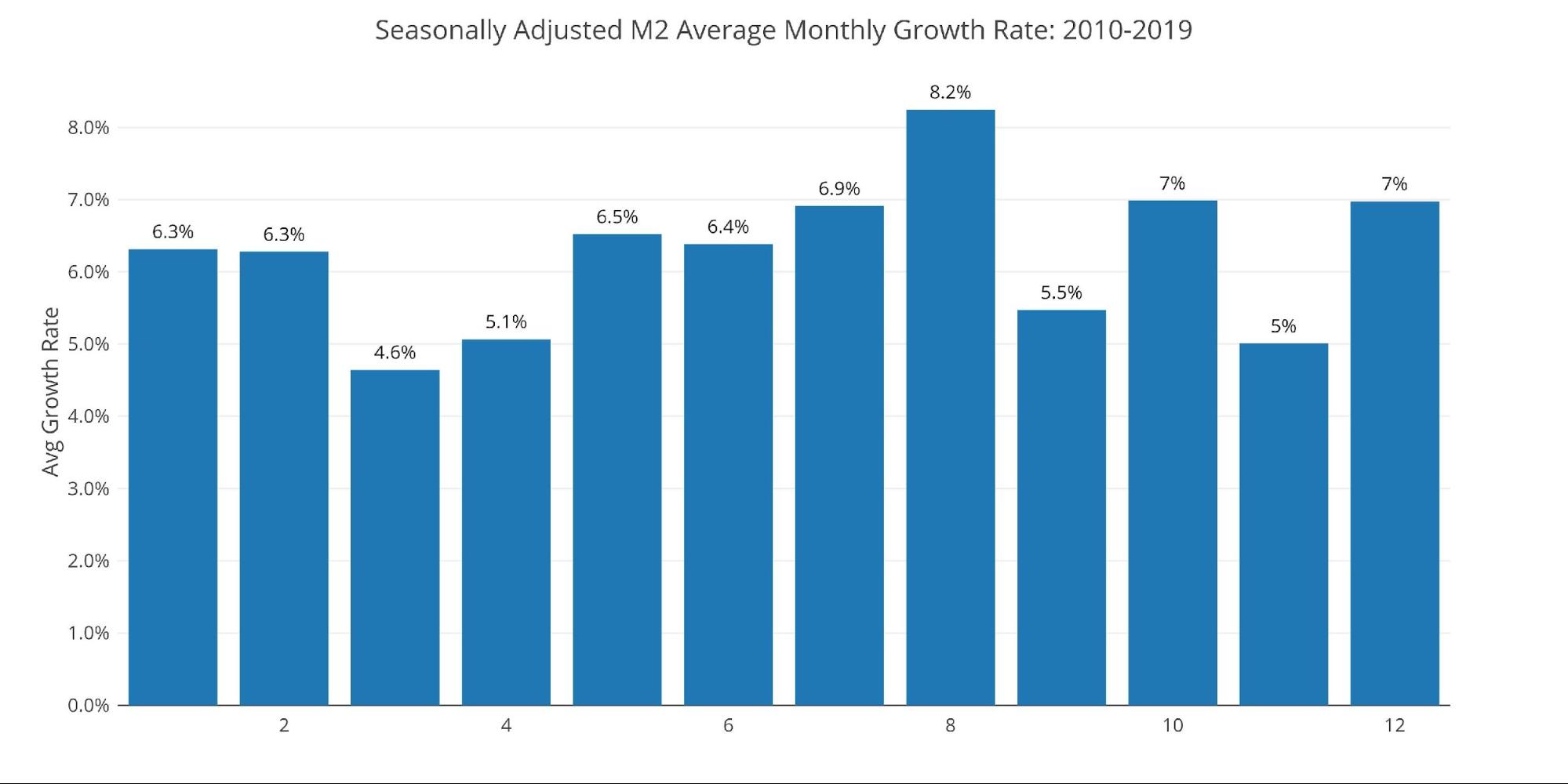

Figure: Growth rate of 2 M2

This is actually well above the March average of +4.6%.

Figure: 3 average monthly growth rates

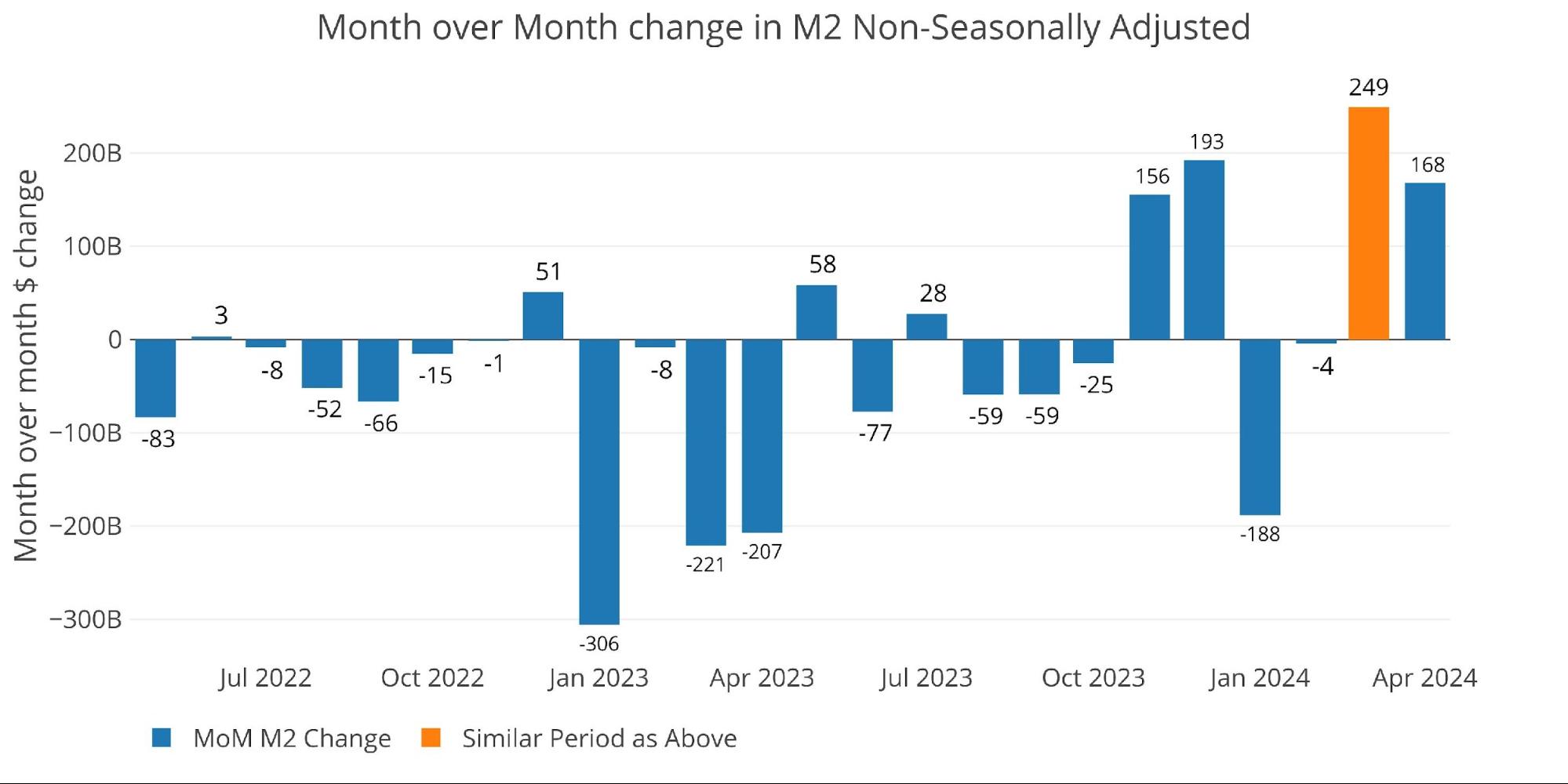

The unadjusted figures show data through early April, with a sharp rise in the two most recent periods.

Figure: 4 Monthly variation of M2 (not seasonally adjusted)

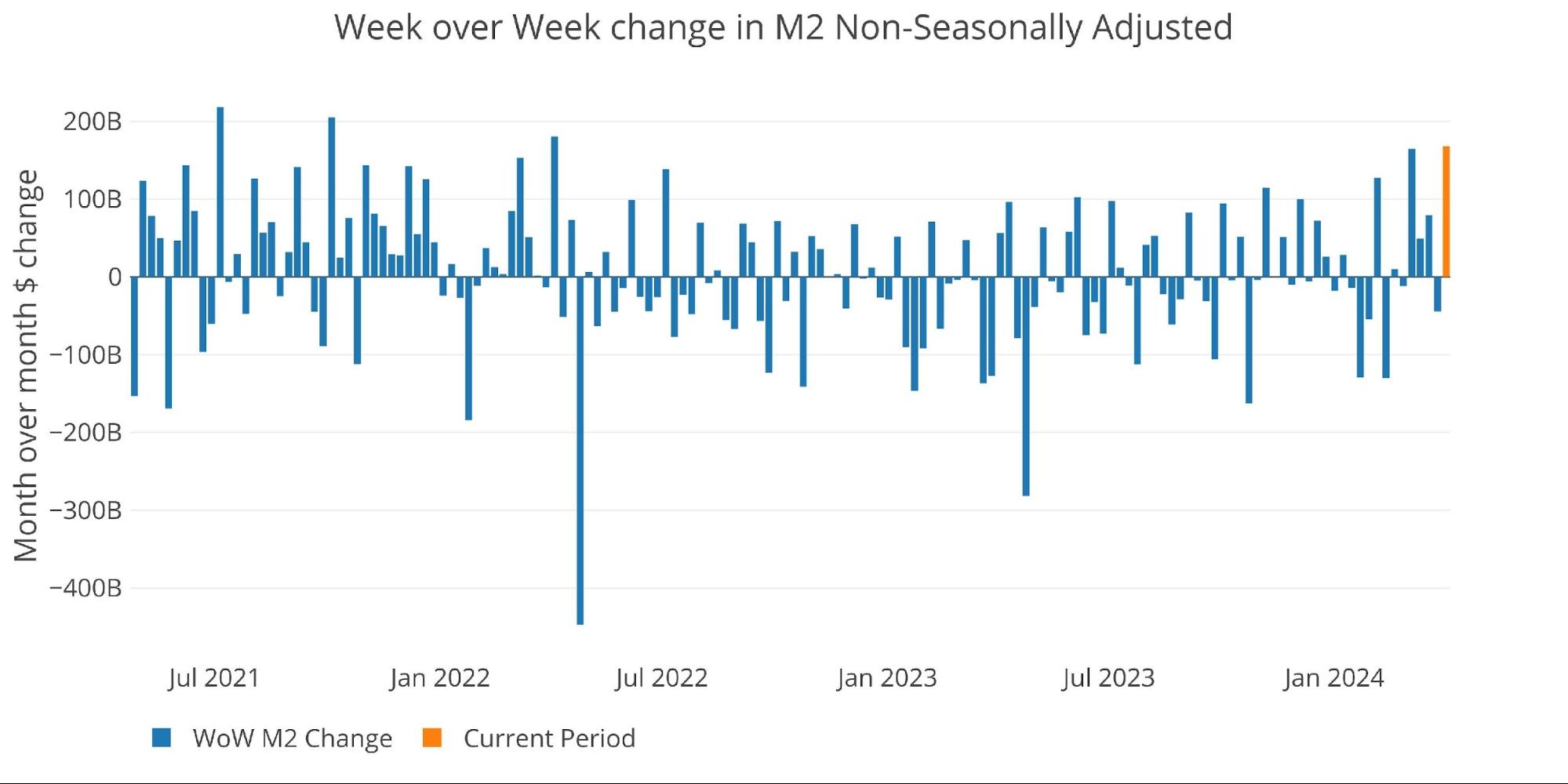

The weekly data below shows activity over the past month in the unadjusted money supply. You can see the big jump in 4 of the last 5 weeks.

Figure: 5 WoW M2 modification

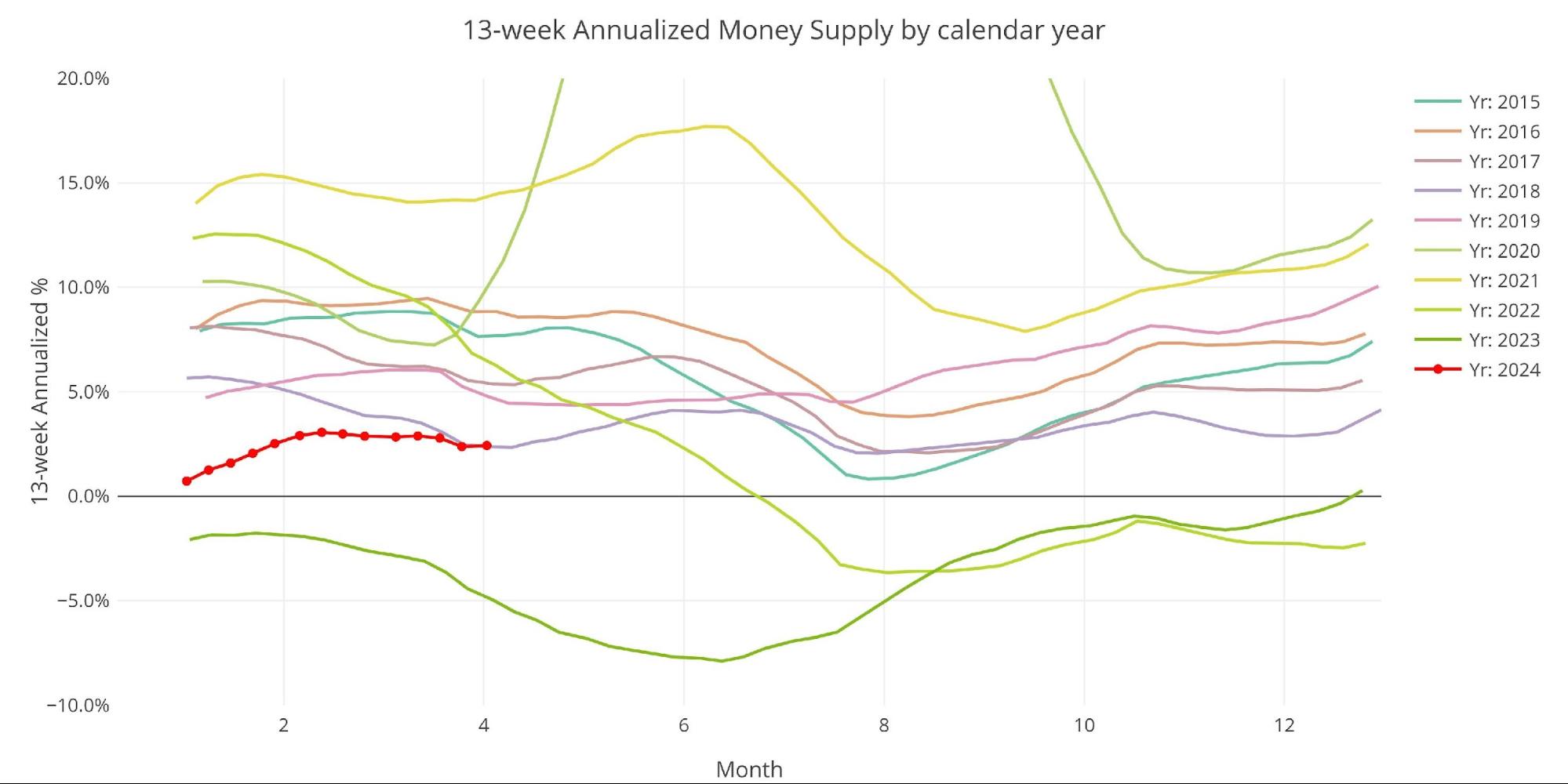

The “Wenzel” money supply over 13 weeks

The late Robert Wenzel of Journal of Economic Policy used a modified calculation to track the money supply. He used a 13-week annualized average growth rate, as defined in his book. The Fed's failures. He specifically used weekly data which was not seasonally adjusted. His analogy was that to know what to wear outside, he wanted to know the current weather, not the average temperatures throughout the year.

The goal of the 13-week average is to smooth out some choppy data without introducing too much history that might prevent someone from seeing what's in front of them. The average growth rate over 13 weeks can be seen in the table below. Deceleration trends are red and acceleration trends are green. The last 10 weeks have been fairly stable compared to recent years.

Figure: 6 Average money supply growth over 13 weeks of WoW

The chart below shows how this year compares to previous years. As we mentioned, the recent period has been rather flat compared to history. The current year is below average for this time of year. The money supply is expected to decline somewhat as summer approaches before rebounding later in the year. However, based on recent weekly data, the money supply could increase in the next report before starting to decline again.

Figure: Overlay of 7 years over 13 weeks

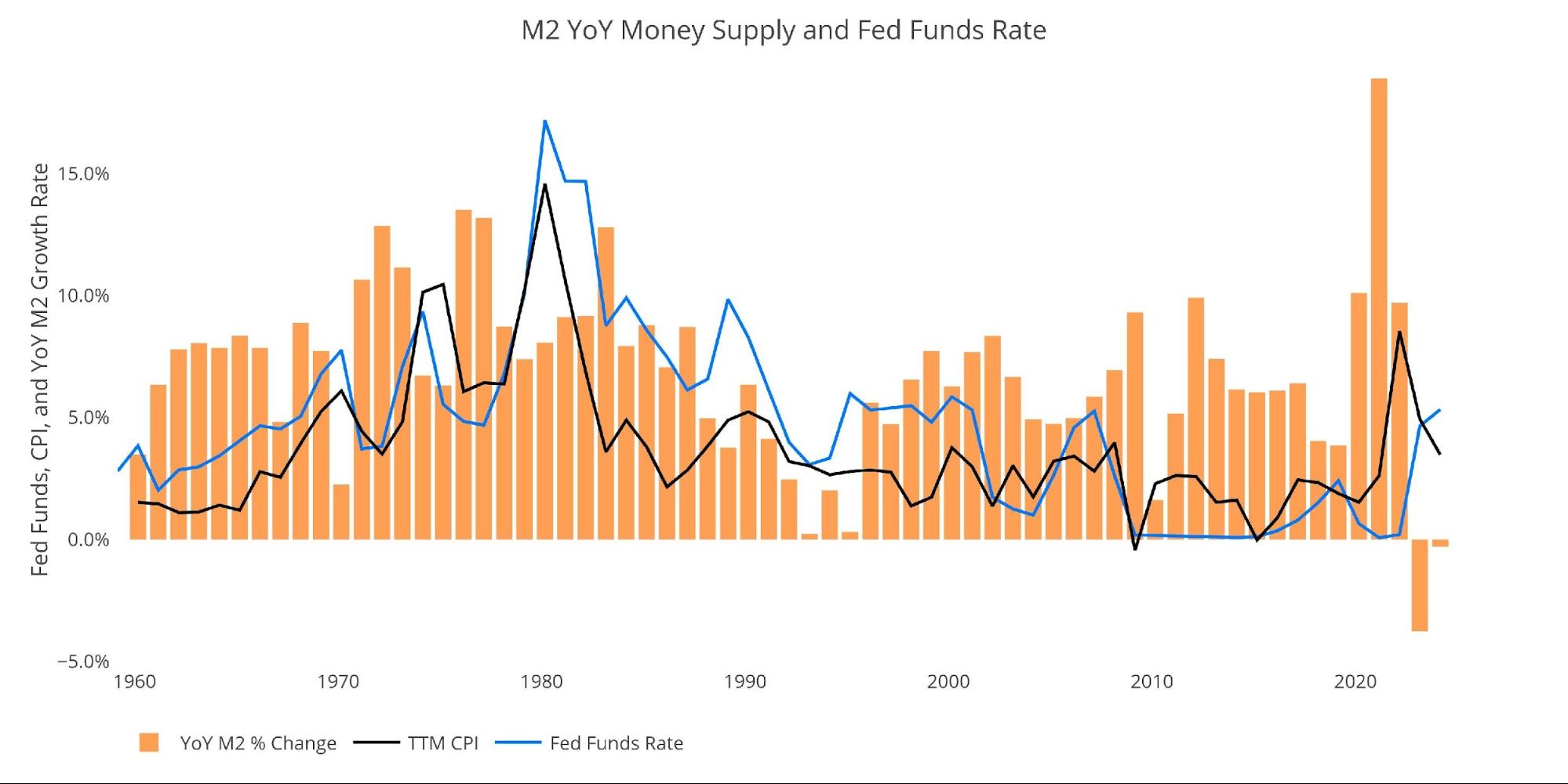

Inflation and money supply

The chart below shows the history of inflation, money supply, and federal funds. As noted, in 1970, inflation operated with a 2-year lag of the money supply. Under these conditions, it is possible that a new surge in inflation is lurking just beneath the surface.

Figure: evolution of M2 over 8 years with the CPI and federal funds

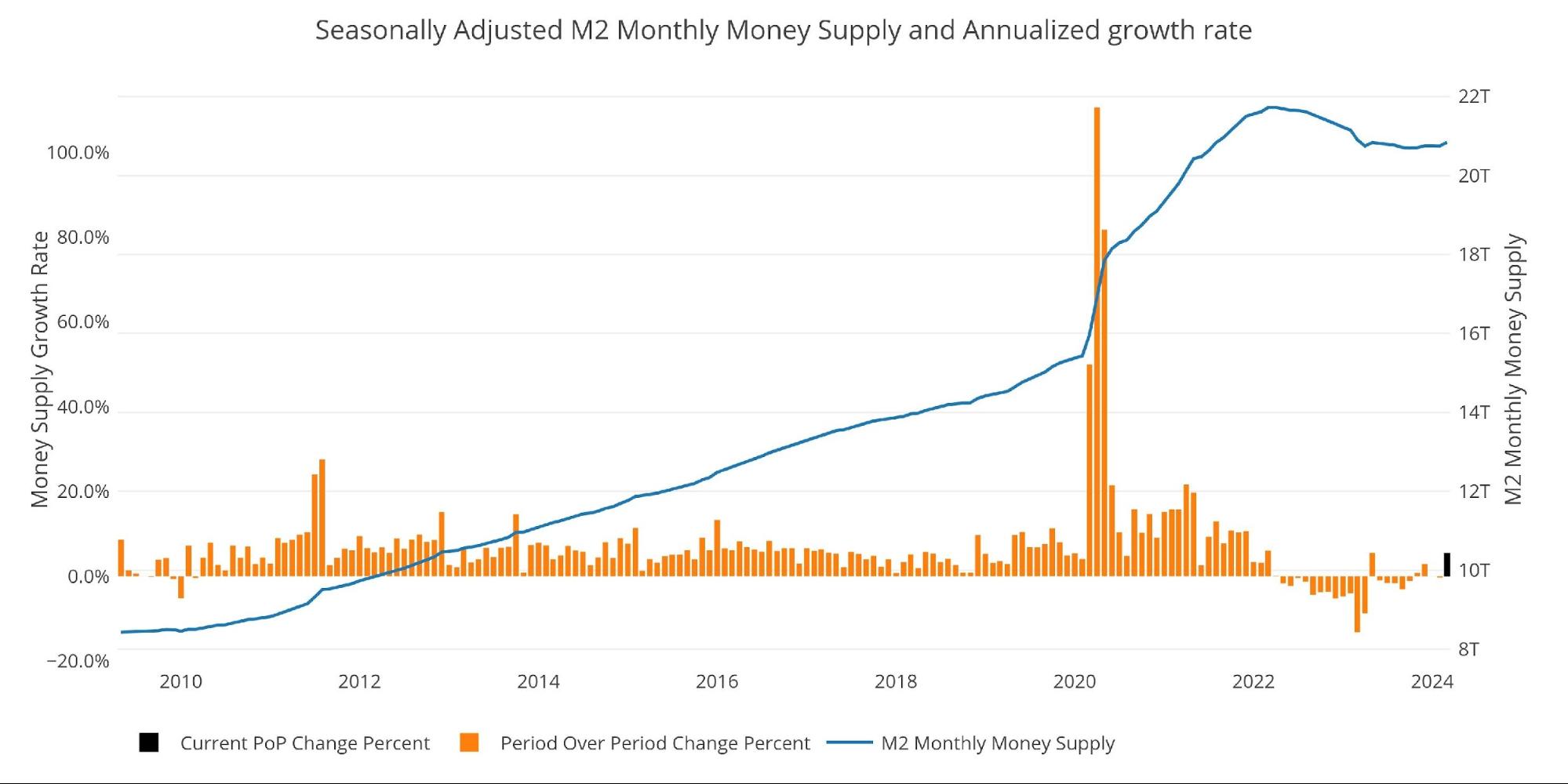

Historical perspective

The charts below are designed to put current trends into historical perspective. The orange bars represent an annualized percentage change rather than a raw dollar amount.

Figure: 9 M2 with growth rate

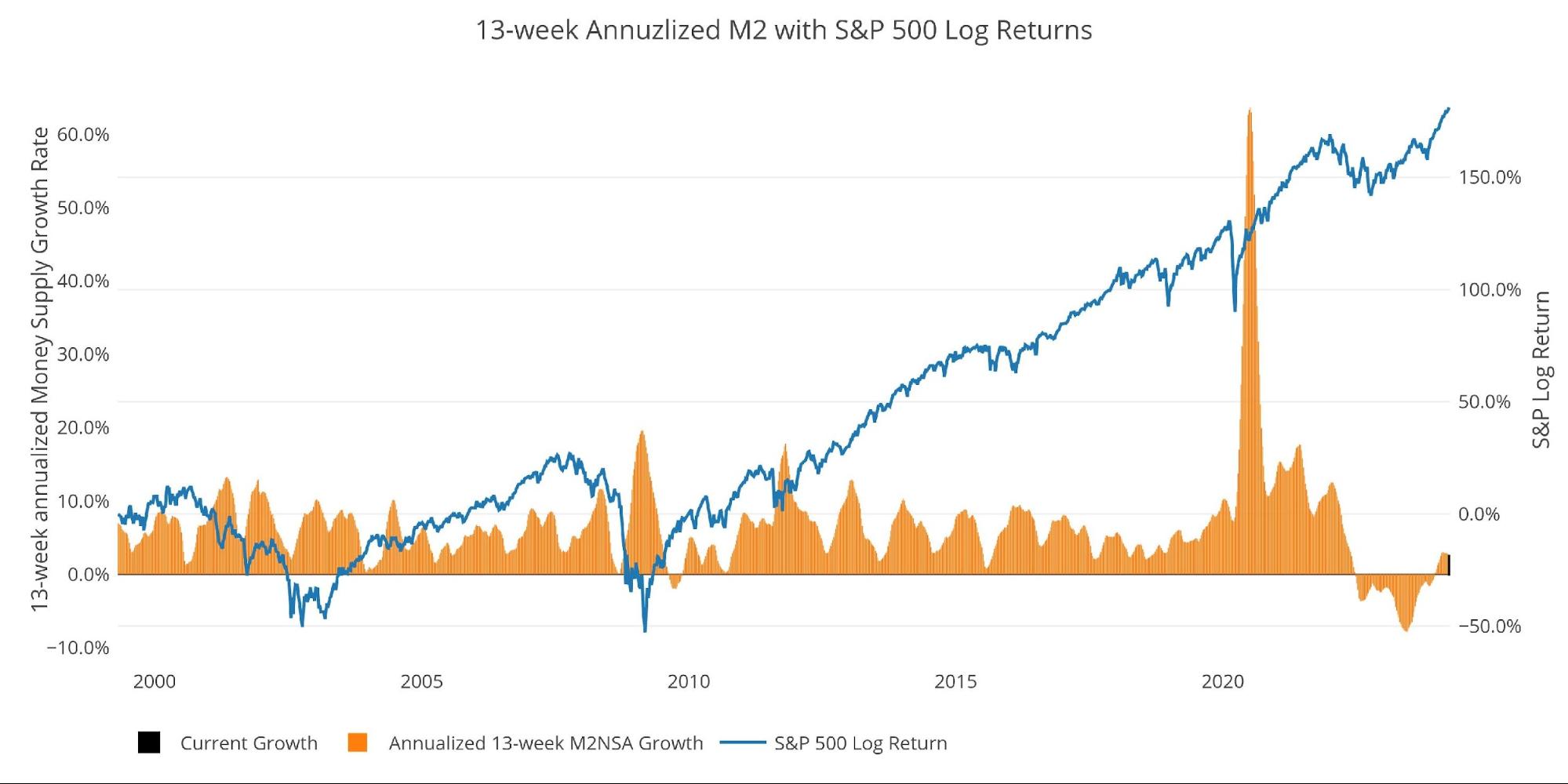

Below is the 13-week annualized average over history. This chart overlays the logarithmic return of the S&P. Mr. Wenzel proposed that sharp declines in the money supply could be a sign of a decline in stock markets. His theory, derived from Murray Rothbard, states that when the market experiences a decreasing (or even negative) money supply growth rate, it can create liquidity problems in the stock market, leading to a selloff.

Although not a perfect predictive tool, many declines in the money supply precede declines in the market. More specifically, the major declines took place in 2002 and 2008, from +10% to 0%. The year 2022 was strongly correlated with a decline in the money supply and the rebound corresponded to the big stock market movement we have seen recently.

Please note that the chart only shows market data through April 1 to align with available M2 data.

Figure: 10 M2 annualized over 13 weeks and S&P 500

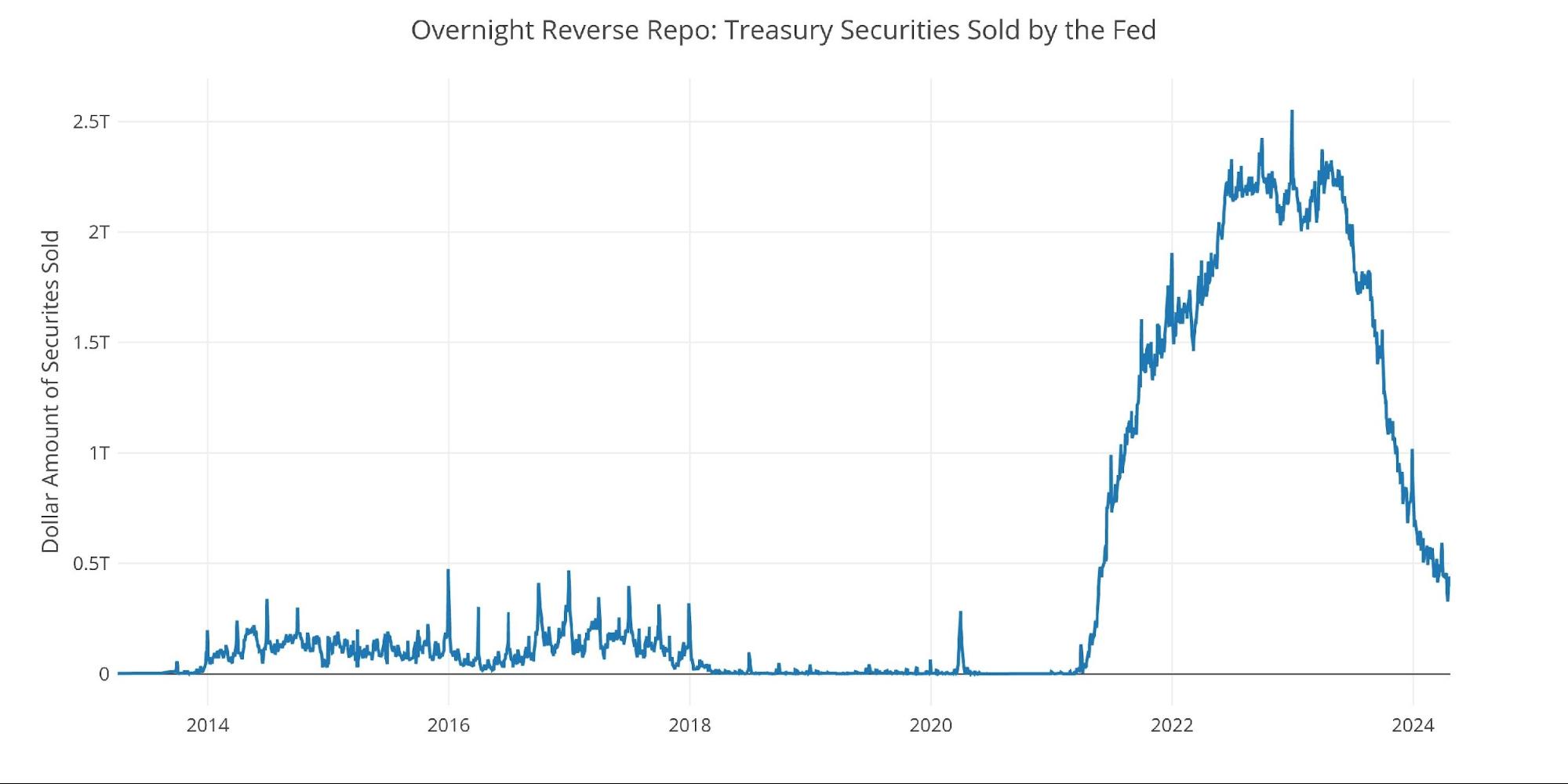

Another consideration is the market for reverse repo at the Fed. It is a tool that allows financial institutions to exchange cash for instruments on the Fed's balance sheet.

Reverse Repos peaked at $2.55 billion on December 30, 2022. Since then, money has been flowing. As the Fed maintains higher interest rates, this decline in repo certainly provides liquidity to the economy, causing the money supply and stock market to rise.

Figure: 11 reverse repurchase agreements by the Fed

Wrap

Money supply can be a leading indicator and help explain stock market action. The money supply fell throughout 2022, bottomed out in early 2023, and has been increasing since. Keeping an eye on the money supply can help understand how much wind is on the stock market.

The data source: https://fred.stlouisfed.org/series/M2SL and also series WM2NS And RRPONSYD. Historical data changes over time, so future article counts may not match exactly. M1 is not used because the calculation was recently changed and backdated to March 2020, skewing the chart.

Data updated: monthly, the fourth Tuesday of the month with a 3-week lag

Most recent data: April 1, 2024

Interactive tables and graphs are still available on the Explore finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Get the most important gold headlines from Peter Schiff once a week – Click here – for a free subscription to his exclusive weekly email updates.

Interested in learning how to buy gold And buy money?

Call 1-888-GOLD-160 and speak with a precious metals specialist today!