The EIGEN airdrop sparked a debate about the divide between private and public markets. The high FDV, points-based meta airdrop fueled by large private rounds is creating structural issues with the crypto industry vibe.

Points programs turning into low-float multi-billion dollar tokens are not a stable equilibrium, but we find ourselves stuck in this meta nonetheless by a confluence of factors: a glut of venture capital, a lack of new entrants and an authoritarian regulator.

The meta around token shows is still evolving, here are the main eras we've seen:

- 2013: PoW fork-and-fair launch meta

- 2017: Meta ICO

- 2020: liquidity mining era (DeFi Summer)

- 2021: NFT coins

- 2024: meta points and airdrop

Each new token distribution mechanism had its advantages and each had its disadvantages. Unfortunately, This One particular meta begins from a place of structural disadvantage for retail, a natural consequence of the merciless regulatory spotlight that hangs over the industry.

Who did this? pic.twitter.com/pvpn8vVCkO

– Takuiten⚡ (@Takuiten) April 30, 2024

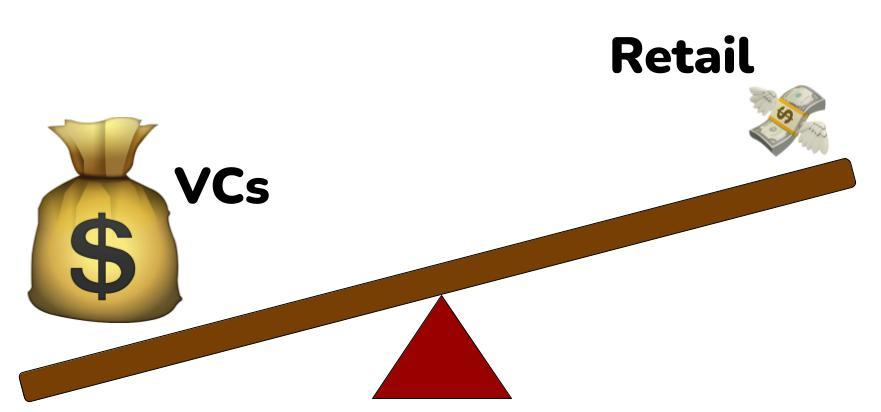

Venture Capital Dollars Abundant Compared to Retail

Right now, there is simply an oversupply of venture capital in the crypto sector. Despite the terrible year 2023 was for VC fundraising, there is still plenty of capital left over from 2021 fundraising, and in general, crypto VC fundraising is a persistent and ongoing activity .

Currently, many well-capitalized venture capital firms are still poised to continue leading funding rounds with multi-billion dollar valuations, meaning crypto startups have the opportunity to stay private for longer and longer . This is of course rational, because if tokens are currently being launched at multiples of their last increase, then even the latest VCs can still find a bargain.

The problem is that by the time a startup releases a public token in the $1-10 billion range, much of the benefit has already been discovered by previous parties – i.e. No one will get rich by buying a $10 billion token.

By structurally disadvantaging public market capital, the mood of the crypto industry is worsening.

People want to get rich with their Internet friends and form strong online communities and friendships around this activity. This is the promise of cryptography, and this promise is currently unfulfilled.

26/ Man *this week alone* we saw three token launches with over $5 billion in overall supply overhang alone

No fucking chance there will be enough institutional offerings to eat up the supply coming into the market.@Arthur_0x I can only buy a limited number of your bagshttps://t.co/fePbu1O7xo

– Regan Bozman (@reganbozman) April 19, 2024

Billions of unlocks, no newcomers

Here are some data points that together should give you pause:

- Vance's calculations indicate that $200-300 billion of venture selling pressure will be unlocked in 2024+2025.

This is the first cycle in which retail has actually taken an interest in unlocks. This is a good thing and I hope they take it into account when making investment decisions. GCR literally had to pull together a bunch of networks to find this information last cycle.

A few points… https://t.co/QXLXDyr8PH

– Vance Spencer (@Pythianism) April 29, 2024

- Coinbase's second quarter report illustrates further evidence that new market entrants are not present, at least not in terms of size.

On Coinbase retail trading volumes:

Still in multiples of the highest of 21', now this can have several interpretations, if you are ultra optimistic you can shout to the sky “WAGMI, it's so early, we are going so high”

But if you look at institutional trading volumes, you notice that they… pic.twitter.com/9z6ZQIql9Z

– Wazz (@WazzCrypto) May 2, 2024

- Since there are not a significant number of new entrants during this cycle, venture capital far exceeds the demand for the fruits of that capital.

25/ TLDR I think a TON of selling pressure is hitting each token with large unlocks that are over 10-20x greater than ANY private round

This is amplified by the fact that these tokens are not THAT liquid – a $1.5 million sale moves Binance. $ARB market 2%+

– Regan Bozman (@reganbozman) March 5, 2024

Since retail primarily owns the long tail of crypto assets, institutional liquidity from Bitcoin ETFs will not appeal to these markets. Recycling capital from crypto-natives who abandon their $14,000 BTC purchases on Larry Fink may support these assets for a while, but it's only internal capital from PVP-capable players who know how unlocks work and how to avoid them.

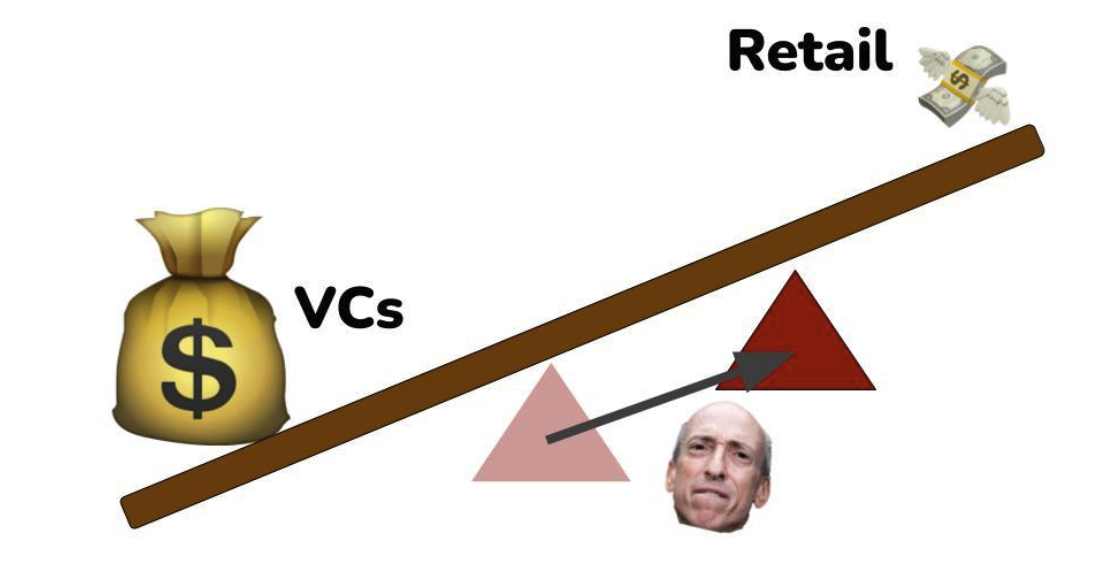

The effect of the SEC

By restricting the ability of startups to more freely raise capital and distribute tokens, the SEC encourages capital to flow into private markets, which are subject to fewer regulatory constraints.

The corrupt and authoritarian nature of the SEC towards the nature of the tokens is weaken the value of capital on public marketsbecause startups cannot exchange their tokens for public market capital without triggering massive aneurysms within their legal teams.

Crypto's March Toward Compliance

Crypto slowly became more compliant as it progressed.

When I first got into crypto, during the ICO craze of 2017, ICOs were presented as a way to democratize investment and access to capital. ICOs have of course become an exploited scam, but it is nonetheless a story that has pushed me and many others to understand the potential that crypto can bring to the world. But the meta-ICO ended when it became clear that regulators viewed these transactions as clearly unregistered securities sales.

The industry then turned to liquidity mining, which followed a similar process.

With each cycle, crypto manages to obscure its method of distributing tokens to the public, and with each cycle, it becomes a little more difficult to hide this process – a process crucial to the decentralization of projects and the nature of our industry.

This The cycle is in the most relentless regulatory spotlight we've ever seen, and so lawyers for venture-backed startups have faced the biggest compliance challenges the industry has ever seen: distribute tokens to the public, without being sued by regulators.

Disturb the balance

Regulatory compliance shifts the pivot from the public-private market to the private side, since startups can choose to simply accept venture capital instead of potentially violating securities laws.

The position of the fulcrum that balances private and public capital is determined by the strength of the chokehold that regulators place on crypto markets.

- If there were no investor accreditation lawsthen this fulcrum would be more balanced.

- If there was a clear regulatory pathway for compliant token issuancethe differences between public and private markets would then be smaller.

- If the SEC wasn't engaged in a war on crypto, we would then have much more fair and orderly markets.

From the SEC won't If we provide clear rules of conduct, we end up with a complicated and convoluted “points” meta that satisfies no one.

Points are unfair and disorderly markets

“Points” give particular users zero clarity about what they actually receive, because if there was ever an explicit articulation of what the points actually are (a claim on tokens), the team would expose themselves as potentially in violation of securities laws ( from the perspective of an authoritarian and corrupt SEC regulator).

The points do not offer any protections to investors, because to provide protections to investors, the process must first have regulatory legitimacy. Following this extremely shitty conclusion we found ourselves in, we discovered the Sybil vs. CommunityThere is a debate in which LayerZero is stuck between a rock and a hard place.

We believe it is in the best interest of the protocol to distribute tokens to sustainable users, not sybil farmers.

If you are a Sybil, you have two options:

– Self-declare Sybil addresses for 15% of your expected allocation. No questions asked. The deadline to do so is May 17.

– Do… pic.twitter.com/Kme9ZKckC7

– LayerZero Labs (@LayerZero_Labs) May 3, 2024

LayerZero recently announced a program for the parachuted Sybils to self-declare their Sybil attack on the incoming LayerZero drop, prompting Kain Warwick to write This thread champion the Sybils as a group of people who have significantly supported LayerZero's measures and improved LayerZero's perceived status in the market.

In reality, there are no boundaries between a member of the community and a Sybil. Since your average crypto participant has no way to engage in private markets, the only way they have to make themselves known encourages engaged and meaningful activity on the platform they want the token for.

With no simple option to let small investors write small checks in early rounds of crypto projects, the current token issuance meta has forced users to Sybil projects they are bullish on. As a result, no “community” comes together to enrich themselves during this cycle, as they did with LINK in 2020 or SOL in 2023. The current token issuance meta does not provide opportunities for communities that gain early exposure to low valuations.

In response, Twitter mob attacks on skydiving startups are increasingly common – a logical consequence of communities not being able to express their desires as valid stakeholders in a project. Big “No taxation without representation!” atmosphere.

This doesn't mean anything other snake in the grass: mercenary capital exploits throwaway tokens. Without the ability for small investors to invest in the early stages of a startup, these highly aligned investors must compete with toxic mercenary farmers for an airdrop, with no notable difference between these two parties.

Inadequate balance

The “points” meta has become too explicit to be sustainable. Both the SEC and the scammers are seizing it, and both will try to exploit it to their advantage.

We will need to move to a different, hopefully more thoughtful, strategy to enrich many early community players while not triggering the wrath of the SEC. Unfortunately, without a regulatory exclusion for token issuance, this remains a pipe dream.

The meta is dead – long live the meta.